From Idle Biofuel Assets to Advanced Fuel Champions: A Turnaround Playbook

- Gaurav Shah

- Sep 6, 2025

- 9 min read

Updated: Jun 16

The renewable-diesel gold rush ended in 2025, and it ended the way booms usually do: with overbuilt capacity, collapsing credit prices and idled plants. For most of the market that is a cautionary tale. For a disciplined operator it is an inventory. The 2024-25 shakeout created a stock of modern, distressed biofuel assets whose sunk capital can be reactivated at a fraction of greenfield cost, and the firms already converting them into SAF and renewable-diesel champions are not reviving failures. They are buying the right skeletons and matching each to the pathway its hardware already supports.

Two Graveyards, Not One

The first discipline is to stop talking about idle biofuel assets as a single category. There are two graveyards, and they could not be more different as investments. The old one holds the first-of-a-kind pilots of the last two decades, cellulosic ethanol, hydrothermal liquefaction, early pyrolysis, plants that stumbled on over-engineered capex, optimistic yields and weak offtake. Most of that hardware is scrap, written down for good reason, and the instinct to buy it cheap is the instinct that keeps losing money. The new graveyard is the one that matters: modern renewable-diesel and biodiesel plants idled in the 2025 margin crush, with sound metallurgy, working pretreatment, real tankage and, often, live permits. The first graveyard is a museum of why first-of-a-kind fails. The second is a clearance sale of perfectly good equipment caught in a bad cycle.

The scale of that cycle is the point. US renewable-diesel and biodiesel capacity overshot past seven billion gallons into clear oversupply; D4 RIN prices fell below 40 cents in early 2025, the lowest since 2019 and down from roughly $1.50 in the boom years, before partly recovering. Biofuel use fell about 20 percent in 2025 and soybean-oil stocks rose 44 percent as demand evaporated. Producers idled hardware: Chevron mothballed two biodiesel plants, and Vertex went furthest, converting its Mobile renewable-diesel facility back to fossil production. That last move is the cautionary note that should sit at the front of every conversion thesis. A brownfield asset does not only convert forwards.

Why Conversion Beats Greenfield

When the cycle turns, and the EPA’s renewable-fuel obligations for 2026 and 2027 require biodiesel and renewable-diesel volumes to climb roughly 60 percent above 2025, the cheapest new capacity is not built. It is converted.

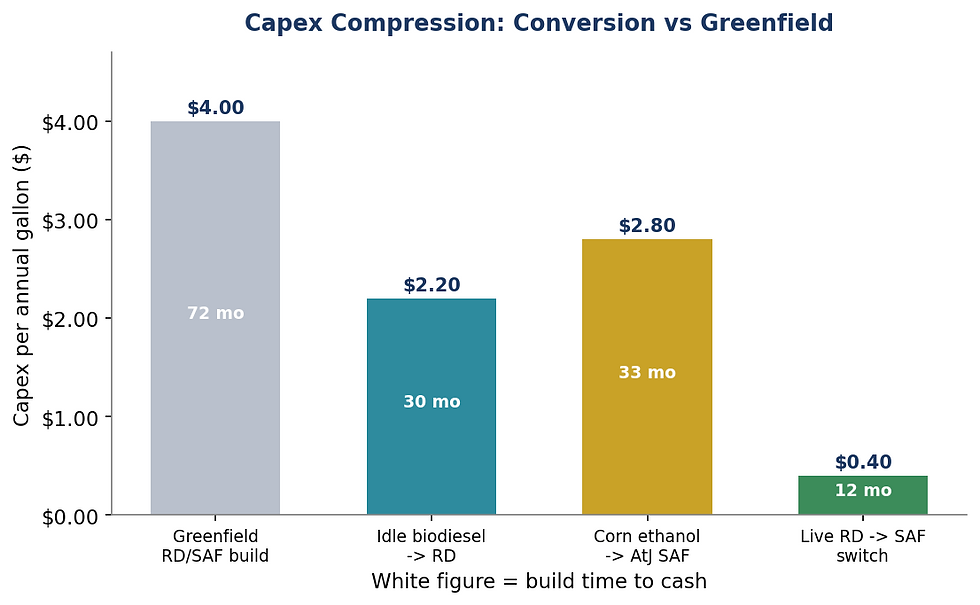

The arithmetic is decisive. A greenfield renewable-fuels plant runs around $4 of capex per annual gallon and takes six years to reach cash. Converting an idle biodiesel plant to renewable diesel costs roughly 45% less and reaches cash in about 30 months, because the tanks, the pretreatment and the hydrotreater shell are already there and already paid for. The boldest play is cheaper still: a live renewable-diesel plant adding the ability to swing output into SAF spends a small fraction of greenfield capex and pays it back in under a year.

Speed and capital efficiency are the alpha here, because in a market where today’s hot pathway can cool in two years, what we have called the velocity of irrelevance, the slow greenfield build is exposed to a policy and price environment that may have moved by the time it starts up.

This is why the moves that matter in 2026 are optionality plays on living assets, not resurrections. Diamond Green Diesel, the Valero and Darling joint venture, completed a SAF project at Port Arthur under budget that lets it swing up to half of its 470-million-gallon renewable-diesel output into SAF. Phillips 66 turned its Rodeo refinery into an 800-million-gallon renewable hub and began producing SAF. Both are buying the right to follow the margin between renewable diesel and jet without building anything new. It is the feedstock-and-product optionality of the margin-shield thesis, expressed in steel.

The Conversion Screen: Champion or Scrap

If the hardware is not the differentiator, what is? The screen that separates a champion from scrap turns on four things the asset either has or does not, and none of them is visible in the purchase price.

Score the candidates and the split is stark. A modern idle renewable-diesel or biodiesel plant scores high on every axis: reusable hardware, a workable feedstock and carbon-intensity position, permits that survived the idling, and a credit-backed offtake into renewable diesel or SAF. An idle corn-ethanol plant scores nearly as well, because its fermenters and tanks are the front half of an alcohol-to-jet facility. The old cellulosic or HTL pilot scores at the bottom on the factor that actually killed it: an unproven, first-of-a-kind process that no retrofit can de-risk. The instinct to chase the cheapest distressed shell is therefore exactly backwards. The bankable target is the asset that already carries hardware, permits, a feedstock position and an offtake, not the one whose only virtue is that nobody else wants it.

The Archetypes That Work

Four turnaround patterns are visibly working in 2026, and each pairs a legacy asset with the pathway its equipment already half-builds.

Legacy asset | Repurposed pathway | Capex saving / IRR uplift | 2026 example (illustrative) |

Idle biodiesel plant | Renewable diesel / HEFA retrofit | ~45% lower capex; ~30 months to cash | FutureFuel Batesville restart |

Corn ethanol plant | Alcohol-to-Jet (AtJ) SAF | +400 to 600 bps IRR vs greenfield AtJ | LanzaJet Freedom Pines; Gevo North Dakota |

Live renewable-diesel plant | RD to SAF switch (optionality) | Sub-year payback on incremental capex | Diamond Green Diesel; Phillips 66 Rodeo |

Old cellulosic / HTL pilot | Scrap or niche co-processing | Usually scrap; rarely a premium niche | Most first-of-a-kind units written down |

The corn-ethanol-to-jet archetype carries the most latent optionality, but it has to be sized honestly, because the gap between what is theoretically possible and what is economic is the whole story of SAF. Global SAF output was only about 1.9 million tonnes in 2025, on the order of 630 million gallons and just 0.6 percent of jet-fuel demand, and it is held back less by technology than by a SAF price that runs up to five times fossil jet and by a wide gap between installed capacity and actual production. Against that backdrop, the roughly 14.6 billion gallons of US ethanol capacity is best read as a theoretical front end rather than a forecast: fully diverting it could in principle yield several billion gallons of SAF, but the binding constraints are economics, capex and competing road-fuel and export demand, not chemistry, and a diversion on that scale is not happening this decade. What is real and bankable today is the marginal play. LanzaJet’s Freedom Pines proved the route at a ten-million-gallon commercial scale with funded ten-year offtake, and Gevo is bolting a thirty-million-gallon SAF unit onto an existing North Dakota ethanol plant rather than building from zero. The value of the ethanol fleet is the low marginal cost of adding SAF, plant by plant, where the offtake and the credit stack already justify it, not a promise of billions of gallons.

Where the Crude Spike Helps, For Once

Unlike an electrolyzer, a converted biofuel asset benefits directly from the 2026 oil environment. Renewable diesel and SAF are physical substitutes for fossil diesel and jet, both oil-linked, so a higher crude price lifts the value of the product these plants make and widens the conversion margin. The offset to watch is the feedstock and the credit: waste-oil and soybean-oil costs are partly oil-linked too, and a soft RIN can erode the gain. But the net direction is favourable, which is precisely why the conversion window is open now. The macro that hurts the merchant hydrogen plant helps the converted lipid refinery, and an allocator should treat the two asset classes oppositely as crude moves.

The Friction That Decides Outcomes

Conversion is not frictionless, and the failures cluster around a few underwriteable risks. Mothballed assets can forfeit grandfathered permits, turning a quick retrofit into a fresh environmental review. Old metallurgy can be mismatched to new feedstocks, surfacing as hidden operating cost rather than visible capex. A stranded ethanol unit is only viable if it can take low-carbon-intensity or cellulosic sugars rather than just its legacy feed, because the carbon score is the credit and the credit is the margin. Skilled operators move on when a plant idles, so ramp-up carries a re-skilling cost. None of these is fatal, but each is a line item, and the Vertex reversal is the reminder that an asset whose converted economics do not clear will simply convert back. Diligence here is not on the hardware that is visible; it is on the permits, the feedstock logistics and the offtake that are not.

How We’d Underwrite It

Buy distress, but screen it hard. Favour modern idle renewable-diesel, biodiesel and ethanol plants over the first-of-a-kind pilot graveyard, and pay for the asset with permits, a feedstock position and an offtake rather than the cheapest shell. Prize optionality: the RD-to-SAF switch on a live plant is the highest-return tonne of new SAF available, and it should be the first thing underwritten, not the last. Treat the corn-ethanol fleet as a strategic, pre-built option on alcohol-to-jet that the mandates are about to make valuable. Underwrite the frictions explicitly, permits, metallurgy, feedstock carbon intensity and workforce, and stress the case for a reverse conversion: if the plant only works on today’s credit prices, it is one policy change from going backwards. In a sector littered with both kinds of graveyard, the discipline is to tell them apart, and to remember that conversion is an act of matching, not resurrection.

What Clears an Investment Committee

Identify which graveyard. A modern idle RD or ethanol plant is convertible; a first-of-a-kind cellulosic or HTL pilot is usually scrap. Do not confuse a low price for a low entry cost.

Underwrite permits, not just steel. Mothballing can forfeit grandfathered rights. Confirm the permit survives before pricing the retrofit.

Solve the feedstock and carbon-intensity position. A cheap shell with the wrong CI earns no credit stack and no margin.

Prize the switch. RD-to-SAF optionality on a live asset is the cheapest new SAF anywhere; weight it first.

Stress the reverse conversion. If the converted economics only clear at current credit prices, model the path back to fossil. Vertex did exactly that.

Idle Biofuel Asset Conversion: Investor FAQ

Why are biofuel plants idle in 2026?

The 2024-25 renewable-diesel gold rush overbuilt capacity past seven billion gallons, D4 RIN prices fell below 40 cents (the lowest since 2019), biofuel use dropped about 20 percent and feedstock-cost and policy uncertainty crushed margins. Producers idled or mothballed plants, and one (Vertex) converted a renewable-diesel facility back to fossil. The result is a stock of modern, distressed but convertible assets.

Is it cheaper to convert an idle biofuel plant than to build new?

Usually, yes. Converting an idle biodiesel plant to renewable diesel costs roughly 45 percent less than greenfield and reaches cash in about 30 months versus six years, because tanks, pretreatment and hydrotreating are already in place. Adding a renewable-diesel-to-SAF switch on a live plant pays back in under a year on incremental capex.

Can a corn ethanol plant be converted to make jet fuel?

Yes, via the alcohol-to-jet (AtJ) pathway, which uses the ethanol plant’s fermenters and tanks as a pre-built front end. LanzaJet’s Freedom Pines proved it commercially at a 10-million-gallon-a-year scale with funded ten-year offtake, and Gevo is adding a 30-million-gallon SAF unit to an existing North Dakota ethanol plant. The US ethanol fleet is a large theoretical front end for SAF, but the binding constraint is economics, not chemistry: global SAF output was only about 1.9 million tonnes (~630 million gallons) in 2025, so the bankable opportunity is marginal, plant-by-plant additions, not a wholesale diversion of the ethanol pool.

Which idle assets are worth converting and which are not?

Modern idle renewable-diesel, biodiesel and ethanol plants score well: reusable hardware, a feedstock and carbon-intensity position, surviving permits and a credit-backed offtake. Old first-of-a-kind pilots (cellulosic, HTL, early pyrolysis) usually do not, because their unproven process is what failed and no retrofit de-risks it. Buy the asset with permits and offtake, not the cheapest shell.

Does the high 2026 oil price help converted biofuel assets?

Yes, directly. Renewable diesel and SAF substitute for oil-linked fossil diesel and jet, so a higher crude price lifts product value and widens the conversion margin. The partial offset is that waste-oil and vegetable-oil feedstock costs are also somewhat oil-linked, and a weak RIN can erode the gain, but the net direction is favourable.

How big is the SAF market in 2026, and why does it matter for conversions?

Small and supply-constrained by economics. Global SAF output was about 1.9 million tonnes in 2025 (~630 million gallons, ~0.6 percent of jet fuel), rising toward 2.4 million tonnes in 2026, with SAF priced up to five times fossil jet and a large gap between installed capacity and actual production. That is exactly why low-capex conversions matter: the cheapest marginal gallon of SAF, an RD-to-SAF switch or an ethanol bolt-on, is far more bankable than a greenfield build into a market that cannot yet absorb high-cost volume.

Methodology: capex (~$4/annual gal greenfield; ~45% lower for idle-biodiesel conversion), build times and payback are illustrative and calibrated to public anchors; EBITDA assumptions $0.80/gal RD and $1.50/gal SAF; conversion-screen scores are Trident’s framework. Companies named (Vertex, Chevron, FutureFuel, Diamond Green Diesel, Valero, Darling, Phillips 66, LanzaJet, Gevo) are named as illustrative examples, not recommendations. Global SAF ~1.9 Mt (~630 M gal) in 2025 per IATA; the 14.6 bn gal ethanol figure is a theoretical ceiling, not a forecast. Sources: EIA; EPA RFS 2026/2027; IATA (SAF output); AlixPartners; Aegis; Biodiesel and Biomass Magazine; LanzaJet and Gevo disclosures. Analysis, not investment advice.

Comments